New installed capacity of offshore wind reached 6.1GW in 2020, 14 times higher than 10 years ago says the Global Wind Energy Council in its latest report. Global installed capacity now sits at 35GW, as stated in the Global Offshore Wind Report 2021.

While delays in permitting lengthened project time for some, the COVID-19 pandemic did not impact the sector too heavily. China is expected to overtake the UK as the country with the largest installed capacity this year.

A factor that will continue to have a big effect on the market is the dramatic fall in the Levelised Cost of Energy from wind projects situated offshore. Prices are becoming more attractive for countries that have the optimal fundamental conditions for offshore wind production and are looking for low-cost, high-capacity renewable energy sources.

The report notes that a key driver of the growth in projects is the increasing number of countries, cities and companies declaring a net zero commitment.

Commitments to meeting Paris Agreement and beyond could be influenced by offshore wind installations

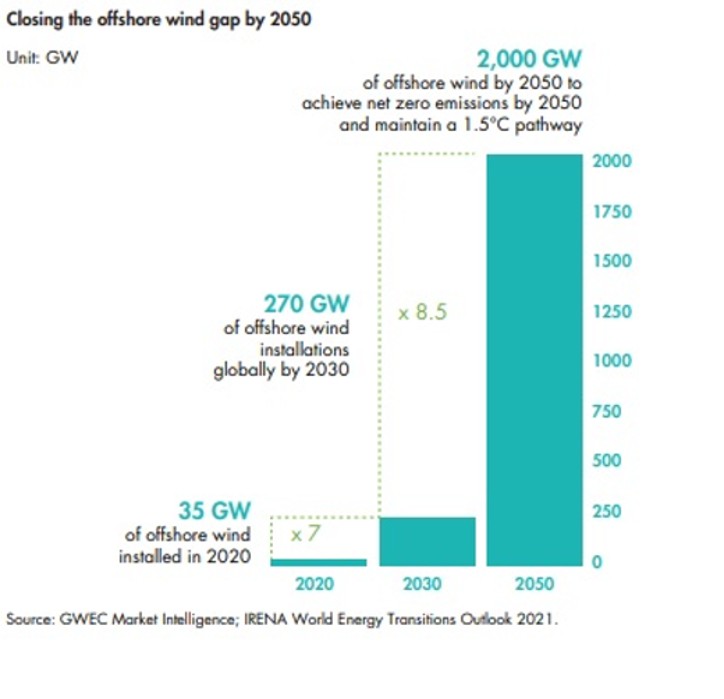

To meet the IEA and IRENA’s 1.5°C scenario, GWEC believes offshore wind capacity will have to be significantly ramped up over the next two decades.

Though 35GW of installed capacity currently exists, primarily in Europe and China, this represents less than 0.5% of global installed capacity. Nonetheless, GWEC points out, the offshore wind resources are formidable. The World Bank has identified more than 71,000GW of technical resource potential available worldwide, which is nearly 10 times the world’s current installed electricity capacity.

The Offshore Wind Resource Hub, launched by GWEC on World Ocean Day in 2021, consolidates territorial maps of fixed and floating offshore wind potential in nearly 100 countries. These illustrate the potential for offshore wind, as an indigenous and sustainable resource, to be distributed in every region of the world, from the Caribbean to East Asia to sub-Saharan Africa.

Based on IRENA’s target of 2,000GW, which would be required to achieve carbon neutrality and sustain a Paris-compliant pathway, GWEC Market Intelligence foresees Asia emerging as the world’s most prominent region for deployment of wind projects offshore, home to nearly 40% of installations by 2050, followed by Europe (32%), North America (18%), Latin America (6%), the Pacific region (4%) and Africa and the Middle East (2%).

Innovations in wind production continue to expand possibilities

Floating wind projects have moved from concept to reality in the last year and fully commercial scale projects are expected by the end of this decade. “Next decade we expect floating wind to compete directly with fixed foundations, partly because floating wind trebles the size of the addressable market,” reads the report foreword.

The report suggests GWEC sees offshore projects as able to compete directly with fixed foundations project “partly because floating wind trebles the size of the addressable market”.

According to the report, the next innovation that will spur wind projects situated offshore to greater deployment is the concept of energy islands. Denmark at the beginning of 2021 approved the creation of an artificial island solely devoted to the creation of energy. It is now moving forward with locations in the North Sea and Baltic Sea identified and survey work commenced. The plan is to have the first phases operational in the early 2030s.

Interest in the subject of hydrogen and Power-to-X (taking surplus renewable electricity from wind, solar or water and converting it into other energy carriers) is growing, which could create routes to market which don’t require a large local power demand. “It is interesting to note that this area is a focus for oil and gas players who bring their considerable experience and skills to the opportunity,” reads the report.

The Global Offshore Wind Report 2021 is available online.

Originally published by Theresa Smith on esi-africa.com